Where US solar demand is headed in 2026 - and how installers can prepare

The US is adding a record 86 GW of new power capacity in 2026, led by solar and battery storage. But the residential market is restructuring fast. Here's where demand is headed, which states are hottest, and what growing installers need to do now.

Payaca is the operations platform for clean tech installation businesses.Book a demo →

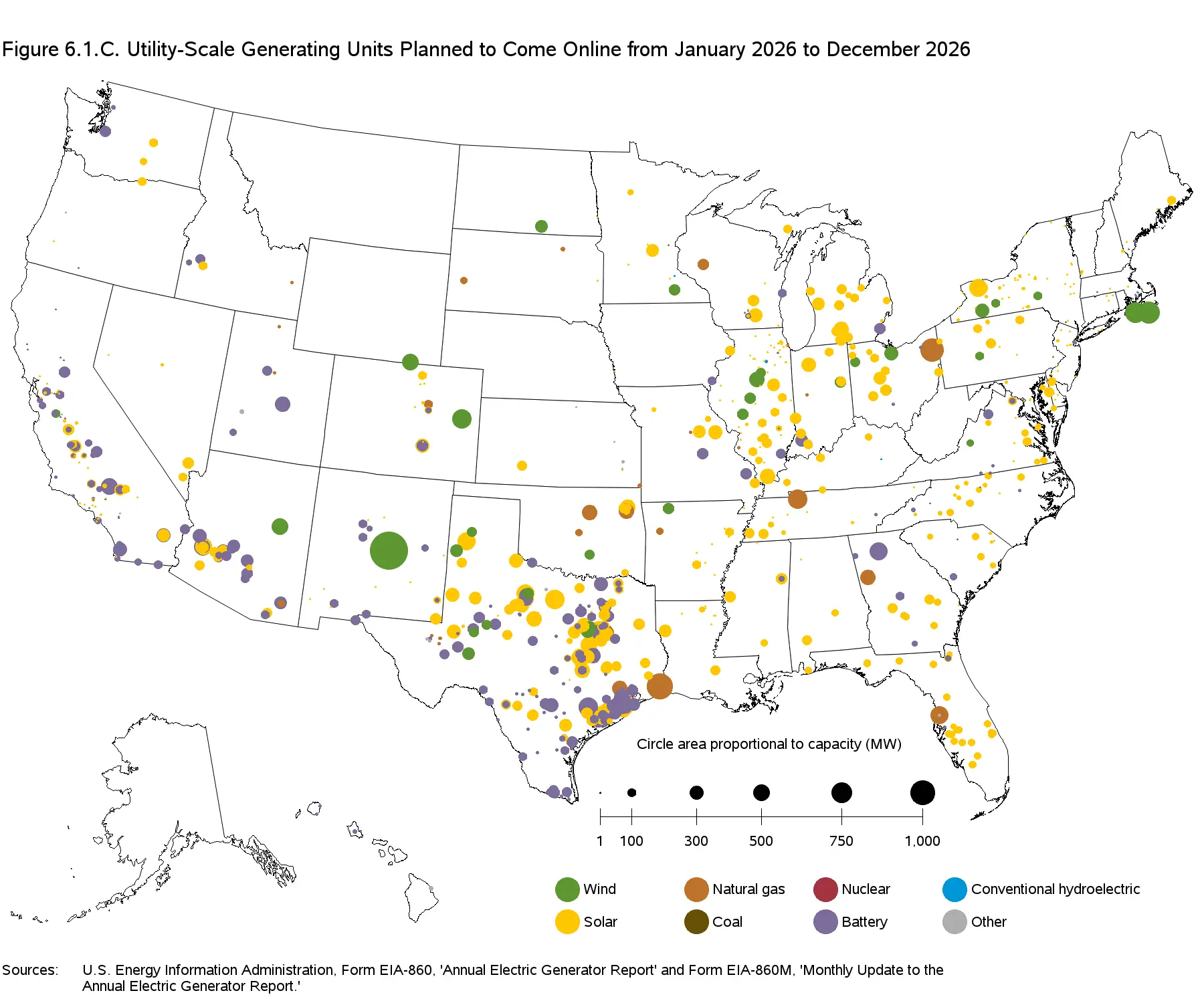

The US energy map is being redrawn. According to the Energy Information Administration (EIA), developers plan to bring a record 86 GW of new power capacity online in 2026. Solar alone accounts for 43.4 GW of that, a 60% increase over last year and the largest single-year addition in history.

Source: U.S. Energy Information Administration, Form EIA-860 and Form EIA-860M

The map tells the story at a glance: yellow dots (solar) and purple dots (battery storage) are spreading across the country, with Texas, the Midwest, and the Southeast seeing enormous investment. But for residential and commercial solar installers, the picture is more nuanced than "everything is booming." The federal tax credit for homeowner-purchased systems expired at the end of 2025, the market is shifting toward third-party ownership models, and battery storage is becoming a must-offer service rather than a nice-to-have.

The installers who understand where demand is concentrating and how the market is restructuring will be the ones who grow through 2026. Those who assume last year's playbook still works will lose ground fast.

Key takeaways

The US is adding 43.4 GW of utility-scale solar and 24 GW of battery storage in 2026, both records

Texas alone accounts for 40% of new utility-scale solar, with Arizona, California, and Michigan rounding out the top four

Residential solar installations are projected to fall around 18% due to the ITC expiry for customer-owned systems

Third-party ownership (TPO) is expected to grow 25% and become the dominant residential model

Battery storage attachment rates are surging, driven by net billing policies and grid reliability concerns

The winners will be installers who diversify into storage, adapt to TPO, and invest in operational capacity

Operational capacity is the constraint - not demand

The installers who grow into 2026 are the ones whose ops scale faster than their pipeline. Book a 20-minute demo to see how Payaca handles solar + storage + TPO workflows in one system.

The headline numbers are staggering. Of the 86 GW of new US power capacity planned for 2026, solar leads at 43.4 GW (51% of total additions), followed by battery storage at 24 GW (28%) and wind at 11.8 GW (14%). Natural gas accounts for just 6.3 GW. The clean energy transition is no longer a forecast; it is the baseline.

This is overwhelmingly utility-scale: large solar farms and grid-scale battery projects. But utility-scale buildout matters for residential installers for three reasons:

Consumer awareness follows infrastructure. When solar farms appear across a state, homeowners notice. Media coverage increases. Solar stops feeling niche and starts feeling inevitable.

State policy follows investment. States attracting utility-scale solar tend to strengthen residential incentives, interconnection standards, and permitting frameworks.

Supply chains mature locally. Equipment availability, skilled labor pools, and installer density all improve in regions with heavy solar investment.

In other words, today's utility-scale hotspots become tomorrow's residential growth markets.

The EIA data reveals clear geographic winners. More than half of the 43.4 GW of new utility-scale solar is concentrated in just four states:

Texas: 40% (~17.4 GW), by far the dominant market, including the 837 MW Tehuacana Creek project with 418 MW of co-located battery storage

Arizona: 6%, sustained desert solar expansion

California: 6%, continued investment despite an already mature market

Michigan: 5%, an emerging Midwest solar state

Battery storage tells a similar story. The 24 GW of new battery capacity is clustering in Texas, California, Arizona, and increasingly across the Southeast and Midwest.

The Midwest is the emerging story

States like Michigan, Ohio, Indiana, and Illinois are seeing significant new solar investment for the first time. For installers in these markets, the window to establish brand presence and operational capacity before competition intensifies is right now.

Here is where the story gets more complex. While utility-scale solar is hitting records, SEIA's Q4 2025 market outlook projects residential installations will contract by around 18% in 2026.

The primary driver: the Section 25D Investment Tax Credit (ITC) for customer-owned residential solar expired on December 31, 2025. Homeowners who purchase systems with cash or a loan no longer receive the 30% federal tax credit.

This triggered a predictable surge in late 2025. According to EnergySage's marketplace data reported by Electrek, the number of homeowners actively working with solar installers surged 205% in the second half of 2025 compared to the same period in 2024 as buyers raced to lock in the credit. That rush is now followed by a demand hangover entering 2026.

But this is a restructuring, not a collapse. Two major forces are offsetting the contraction:

TPO providers (lease and PPA companies) can still claim the commercial 48E investment tax credit through 2027. That means homeowners can still access solar at zero upfront cost through a lease or power purchase agreement. They just cannot claim a personal tax credit on a purchased system.

Market analysts expect TPO to grow 25% in 2026, with TPO projected to capture up to 69% of residential installations, up from roughly 45% in 2025. Companies like Sunrun, Palmetto, and GoodLeap are expanding aggressively.

What this means for installers: If your business model relies entirely on cash and loan sales, 2026 will be painful. The companies adapting to TPO partnerships or offering their own financing options are positioned to capture demand that cash-purchase installers are losing.

Residential battery storage grew 51% year-over-year in 2025, reaching 3.1 GWh according to SEIA's Energy Storage Market Outlook. Overall US storage deployments are projected to reach 70 GWh in 2026, up from 58 GWh in 2025.

The drivers are structural, not temporary:

Net billing policies in states like California have made batteries essential for maximizing solar value. Battery attachment rates have surged since California's transition from net metering to net billing.

Grid reliability concerns in states like Texas and Florida are driving homeowner interest in backup power.

Virtual power plant (VPP) programs in Massachusetts, Texas, Arizona, and Illinois are creating new revenue streams for battery owners.

51%

Residential battery storage growth in 2025 (year-over-year)

For solar installers, battery storage is no longer a premium upsell. It is a core competency. The average deal value on a solar-plus-storage project is significantly higher than solar alone, and customers who buy storage are more engaged, more likely to refer, and more likely to buy additional services.

Based on the convergence of utility-scale investment, residential demand, policy environment, and storage growth, here are the five states where solar installers have the strongest growth opportunity in 2026:

Texas is in a category of its own. It leads in utility-scale solar (40% of national additions), has a strong residential market driven by high electricity costs and grid reliability concerns, and benefits from relatively efficient permitting. The ERCOT grid's reliability issues continue to drive consumer interest in solar-plus-storage. If you are not in Texas and have the capacity to expand, this is the market to watch.

Despite being a mature market, California remains the largest residential solar state by installed capacity. The shift to net billing has transformed the sales conversation. It is now fundamentally about solar-plus-storage rather than solar alone. Installers who have adapted to this reality are thriving. Those still selling solar-only systems are struggling.

Florida consistently ranks in the top three for residential installations. High electricity costs, hurricane-driven storage demand, and strong population growth make it a durable market. The absence of a state income tax means the federal ITC changes hit differently here, making TPO models especially important.

Arizona benefits from exceptional solar resources, significant utility-scale investment, and growing residential demand. The state's net metering policies are evolving, which creates both challenges and opportunities for installers who can articulate the battery storage value proposition clearly.

This is the breakout story of 2026. Michigan alone accounts for 5% of new utility-scale solar capacity, and the broader Midwest corridor is seeing its first wave of serious solar investment. Residential markets here are earlier-stage, which means less competition, lower customer acquisition costs, and first-mover advantages for installers who establish presence now. Virtual power plant programs in Illinois are adding additional demand drivers.

If you are not already quoting solar-plus-storage on every residential project, start now. The demand is there, the margins are better, and customers increasingly expect it. Storage also opens doors to commercial projects, VPP programs, and recurring monitoring revenue.

The ITC expiry for customer-owned systems means your sales pitch needs to evolve. Whether you partner with TPO providers, offer in-house lease options, or simply refine your cash-purchase value proposition around rising utility rates, the old "30% tax credit" headline is gone. The new pitch is about long-term energy costs and grid independence.

The installers who struggle during demand surges are not the ones lacking leads. They are the ones whose operations cannot keep up. Quoting takes too long, scheduling falls apart, permit tracking is manual, and customer communication drops. This is where businesses lose money: not from a lack of demand, but from an inability to convert and deliver efficiently.

The operational bottleneck

When demand surges in your market, having tight operations (fast quoting, automated follow-ups, real-time scheduling, and efficient permit tracking) is the difference between scaling revenue and just scaling chaos. The time to build that infrastructure is before you need it, not during a rush.

If you have the capacity to expand geographically, the Midwest corridor and parts of the Southeast represent significant first-mover opportunities. Utility-scale investment is creating awareness, but residential installer density is still low. The companies that build brand presence and local relationships now will have a structural advantage as these markets mature.

A homeowner who installs solar today might need a battery in two years, an EV charger in three, and a panel expansion in five. The installer who maintains that relationship captures all of that revenue. The one who treats each install as a one-off transaction does not. Monitoring contracts, maintenance agreements, and proactive outreach to existing customers are how you build a durable business, not just a busy one.

2026 is not a year of simple growth or simple decline for US solar installers. It is a year of restructuring. The total addressable market is expanding, driven by record utility-scale investment, surging battery demand, and long-term consumer interest in energy independence. But the way that market is accessed is changing, and the companies that adapt their business model, their service offerings, and their operational capacity will be the ones that capture it.

The EIA's map of 2026 capacity additions shows solar and storage spreading across the country. The demand will be there. The installers who've built the operations and service mix to capture it will grow. Those still running last year's playbook will watch it pass them by.

US solar installers don't have one national permitting clock - they have as many as they have AHJs. Here's what that variance actually costs a growing install business, backed by NREL data.

A practical breakdown of where UK solar installer margin is won and lost - from survey to DNO energisation. Covers the real cost of quoting, MCS and DNO admin, on-site overruns, and how growing installers protect 20% margins as volume scales.

Pipedrive is the SMB sales pipeline that lots of US solar and battery installers reach for first. It does the sales side well and stops at deal-closed. A side-by-side workflow walkthrough through permitting, interconnection, ITC documentation, install and PTO.

Source: U.S. Energy Information Administration, Form EIA-860 and Form EIA-860M

Source: U.S. Energy Information Administration, Form EIA-860 and Form EIA-860M